Ifrs 9 Deutsch

International Financial Reporting Standard 9 (IFRS 9) is a new accounting standard set to replace International Accounting Standard 39 (IAS 39) It introduces a new approach to accounting for financial instruments and is expected to become effective in December 18 The three main areas covered by IFRS 9 are.

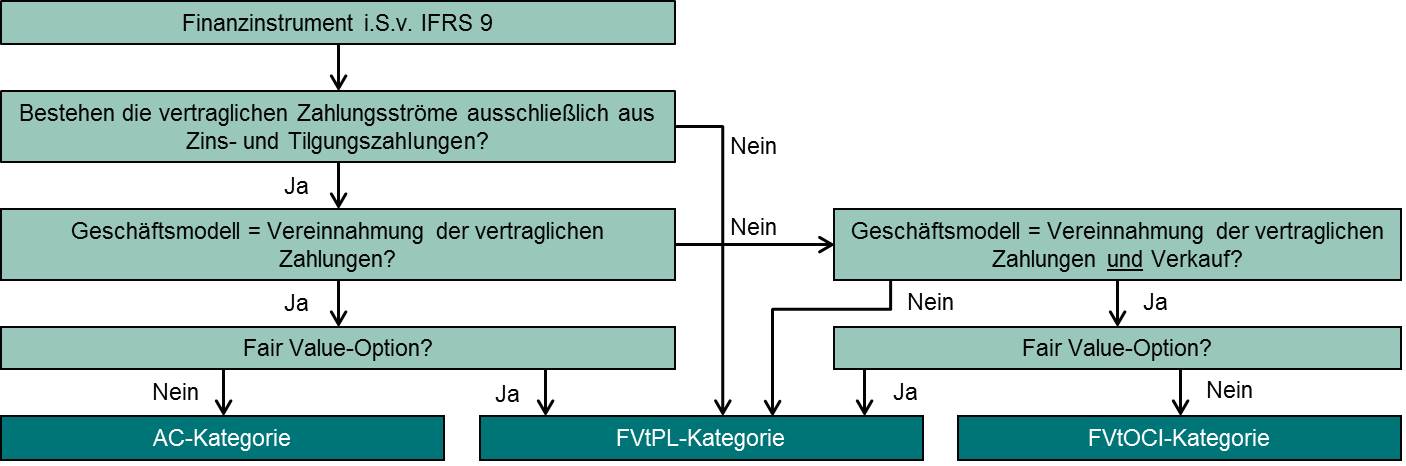

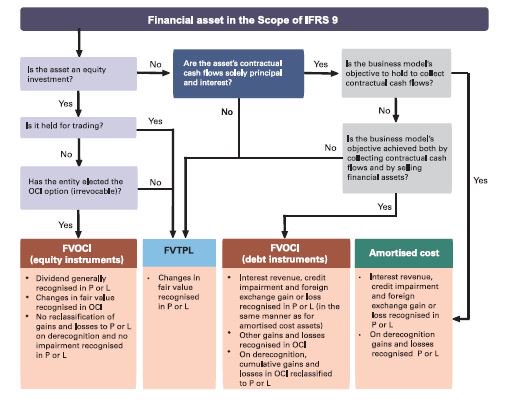

Ifrs 9 deutsch. Draft amendments to ifrs 9 financial instruments 9 draft amendments to ias 39 financial instruments recognition and measurement 12 approval by the board of exposure draft interest rate benchmark reform published in may 19 15 basis for conclusions on the exposure draft 16 i nterest r ate b enchmark r eform —p roposed amendments. Classification of financial assets under IFRS 9(A) At amortised cost An asset (other than equity instrument) that meets the below mentioned conditions The asset is held within a business model whose objective is to hold assets in order to collect contractual cash flows;. The contractual cash terms of the financial asset give rise to cash flows on specific dates that are solely payments of principal and interest on the principal amount outstanding;.

IFRS 9 Navigating the Transition IFRS 9, Financial Instruments, as issued by the IASB on July 24, 14 (IFRS 9 (14), supersedes all other prior versions of IFRS 9 The standard is effective for annual periods beginning on or after January 1, 18, with earlier adoption permitted While IFRS 9 (14) must be applied retrospectively in accordance with IAS 8, Accounting Policies, Changes in Accounting Estimates and Errors, the standard contains specific transition provisions. Https//wwwcpdboxcom/This is just the short executive summary of IFRS 9 and does NOT replace the full standard you can see the full text on IFRS Foundati. And (b) paragraph B63 of IFRS 15 on consideration in the form of salesbased or usagebased royalties on licences of intellectual property (Example 4) Example 1—Collectability of the consideration.

19 edition (PDF 29 MB) 18 edition (PDF 27 MB) Supplements to annual Illustrative disclosures COVID19 supplement (PDF 25 MB) IFRS 12 supplement (PDF 12 KB) IFRS 15 supplement (PDF 15 MB) IFRS 16 supplement (PDF 18 MB) Annual Disclosure checklists edition (PDF 25 MB) 19 edition (PDF 26 MB) 18 edition (PDF 19 MB). IFRS 9 replaces IAS 39 Financial Instruments Recognition and Measurement, and is effective for annual periods beginning on or after January 1, 18 Earlier application is permitted IFRS 9 uses an expected credit loss (ECL) model which replaces the current incurred loss model under IAS 39 The IFRS 9 impairment requirements aim to address concerns raised during the financial crisis relating to the current IAS 39. Published on November 18, 17 November 18, 17 • 21 Likes • 0 Comments Deutsch (German) English (English) Español (Spanish).

IFRS 9 and CECL Credit Risk Modelling and Validation A Prac £4761 starrating (13) International Financial Reporting Standards (IFRS) Deutsch £2495 starrating. The revised manual takes into account the new approach set out in IFRS 9 to impairments of bank assets and classifying financial instruments The assessment of provision levels on credit exposures follows the IFRS 9 staging model, which introduces the concept of “significant increase in credit risk since initial recognition” of a financial. IFRS1 Australia, New Zealand and Israel have essentially adopted IFRS as their national standards2 Brazil started using IFRS in 10 Canada adopted IFRS, in full, on Jan 1, 11 Mexico will require adoption of IFRS for all listed entities starting in 12 Japan is working to achieve convergence of IFRS and began permitting certain qualifying.

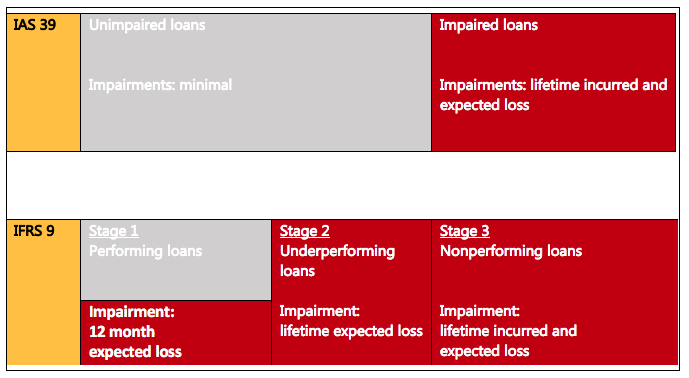

IFRS 9, which will replace IAS39 for the accounting periods beginning on or after 1 January 18 8, requires the measurement of impairment loss provisions based on an ECL accounting to be rather than on an incurred model loss accounting model 6 The EBA welcomes the move from an incurred loss model to an ECL model under IFRS 9 9 IFRS 9 is,. IFRS 9 Financial Instruments has brought fundamental changes to financial instruments accounting in recent years Our materials will help you understand the requirements of this standard as they relate to your company, as well as offering insights and guidance on the application of IFRS ® Standards. IFRS 9 states that firms shall apply a definition of default consistent with the definition used for internal credit risk management purposes However, there is a rebuttable presumption that a default does not occur later than when the instrument is 90 days pastdue.

With the help of Capterra, learn about IFRS 9 Impairment Solution, its features, pricing information, popular comparisons to other Banking Systems products and more Still not sure about IFRS 9 Impairment Solution?. IFRS 9 – the end of weighted average accounting?. IFRS 9 – Classification and measurement At a glance On July 24, 14 the IASB published the complete version of IFRS 9, Financial Instruments, which replaces most of the guidance in IAS 39 This includes amended guidance for the classification and measurement of financial assets by introducing a.

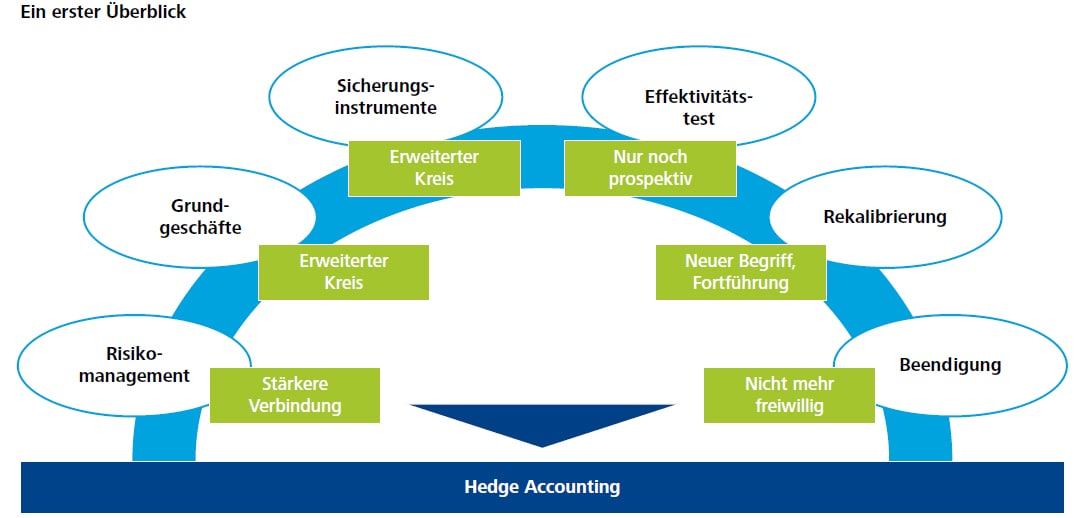

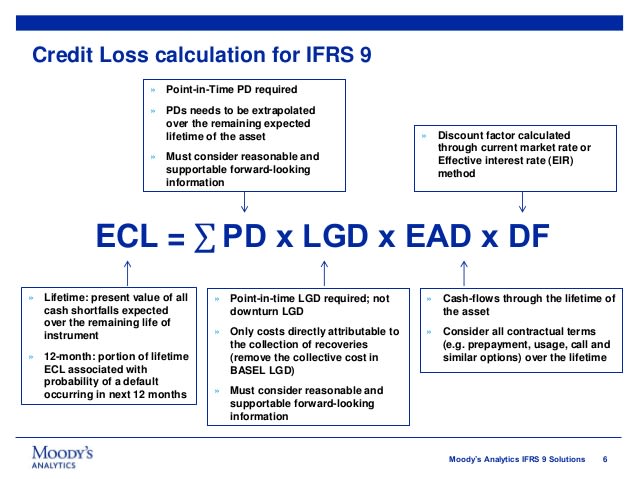

IFRS 9 Hedge Accounting Erweiterung der zulässigen Grundgeschäfte Veränderte Buchungslogik für (nicht designierte) Wertkomponenten von Sicherungsinstrumenten Wegfall der freiwilligen Dedesignation Erhöhte Offenlegungs und Dokumentations anforderungen Rekalibrierung einer Sicherungs beziehung Vereinfachungen beim Effektivitäts nachweis. A significant new feature of IFRS 9 is the requirement to record loss allowances based on an expected credit loss model, being substantially more forward looking in nature, compared to the incurred loss accounting model of IAS 39 A uniform model is applied for Financial assets measures at amortized cost;. And reasonable and supportable information that is available without undue cost or effort at the reporting date about past events, current conditions and forecasts of future economic conditions.

Technical resources on the International Financial Reporting Standards (IFRS) – get started now with practical guidance, latest thinking and tools Skip to the content EY Homepage Search Close search See all results in Search Page No results have been found Recent searches (container). Check out alternatives and read real reviews from real users. Der International Financial Reporting Standard 9 (IFRS 9) löst den derzeitigen Standard IAS 39 ab und wird ab für alle nach IFRS bilanzierenden Unternehmen verbindlich Die finale Fassung von IFRS 9 enthält neben den neuen Regelungen zur Klassifizierung und Bewertung von Finanzinstrumenten und zur Bilanzierung von Sicherungsverhältnissen auch erstmals neue Vorschriften zur.

Das Wichtigste in Kürze Mit dem jüngst veröffentlichten IFRS 9 (14) Finan zinstrumente werden neben den Vorschriften für Wertminderungen auch die Klassifizierung und Bewer tung von Finanzinstrumenten endgültig geregelt. International Financial Reporting Standard 9 (IFRS 9) is a new accounting standard set to replace International Accounting Standard 39 (IAS 39) It introduces a new approach to accounting for financial instruments and is expected to become effective in December 18 The three main areas covered by IFRS 9 are Classification and measurement of financial instruments. Example 9 Reconciliation of changes in property, plant and equipment These examples are based on illustrative examples from the IFRS for SMEs They represent how reconciliation of gross carrying amount, accumulated depreciation and carrying amount of property, plant and equipment might be tagged using detailed XBRL tagging Inline XBRL;.

IFRS 9 states that firms shall apply a definition of default consistent with the definition used for internal credit risk management purposes However, there is a rebuttable presumption that a default does not occur later than when the instrument is 90 days pastdue. IFRS 9 behandelt drei großen Themen, die in drei Phasen erarbeitet wurden Deshalb werden sie auch jetzt noch so bezeichnet Phase 1 behandelt das Thema Klassifizierung und Bewertung von Finanzinstrumenten, Phase 2 das Thema Wertminderung, Phase 3 die Bilanzierung von Hedgegeschäften Entwicklung IFRS 9 wurde am 24. IFRS 9 is an International Financial Reporting Standard published by the International Accounting Standards Board It addresses the accounting for financial instruments It contains three main topics classification and measurement of financial instruments, impairment of financial assets and hedge accounting The standard came into force on 1 January 18, replacing the earlier IFRS for financial instruments, IAS 39.

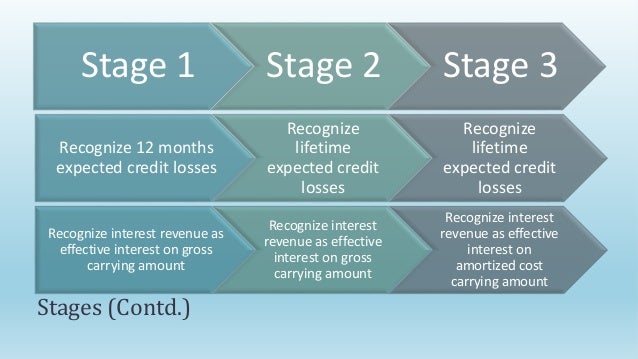

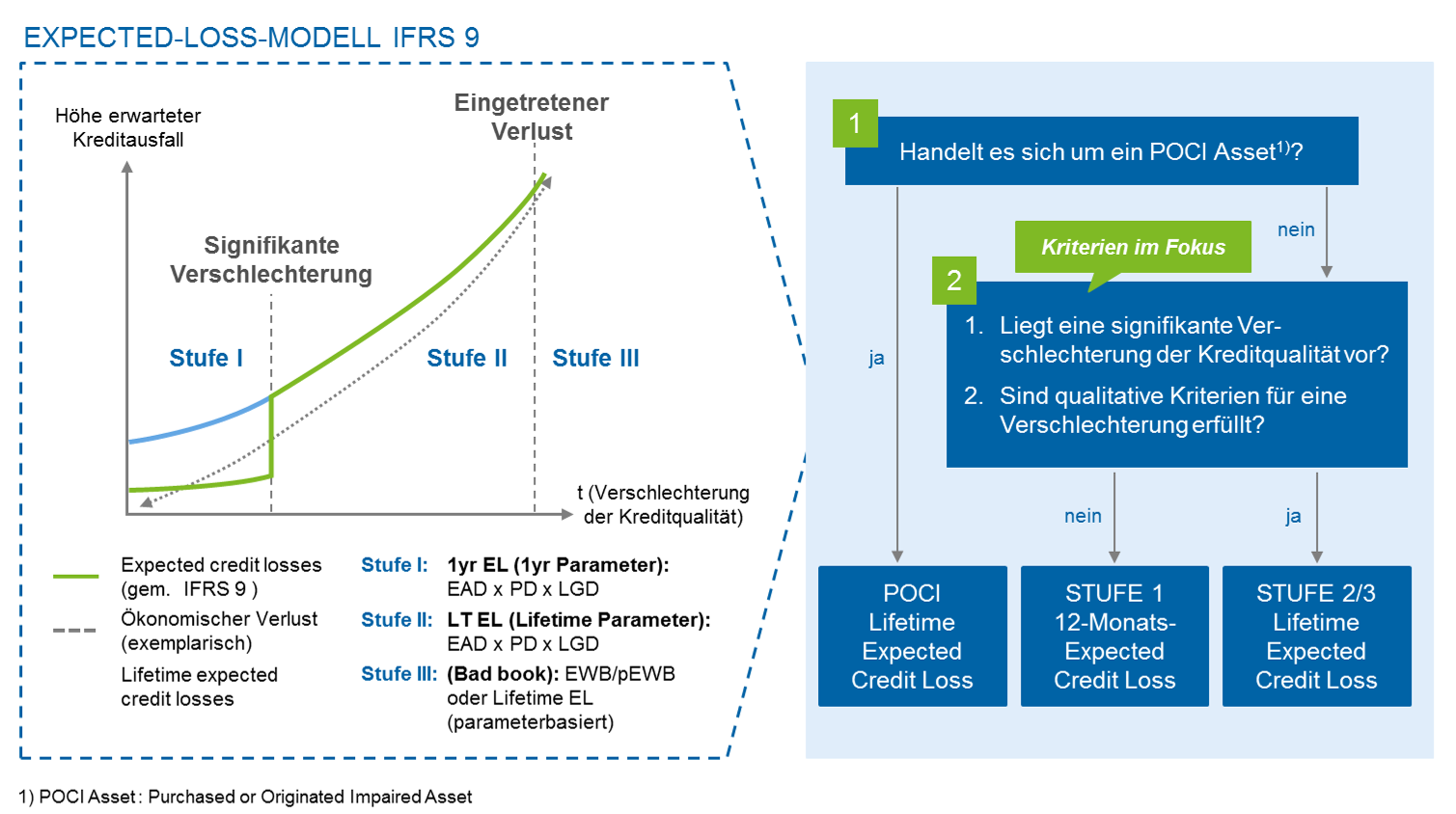

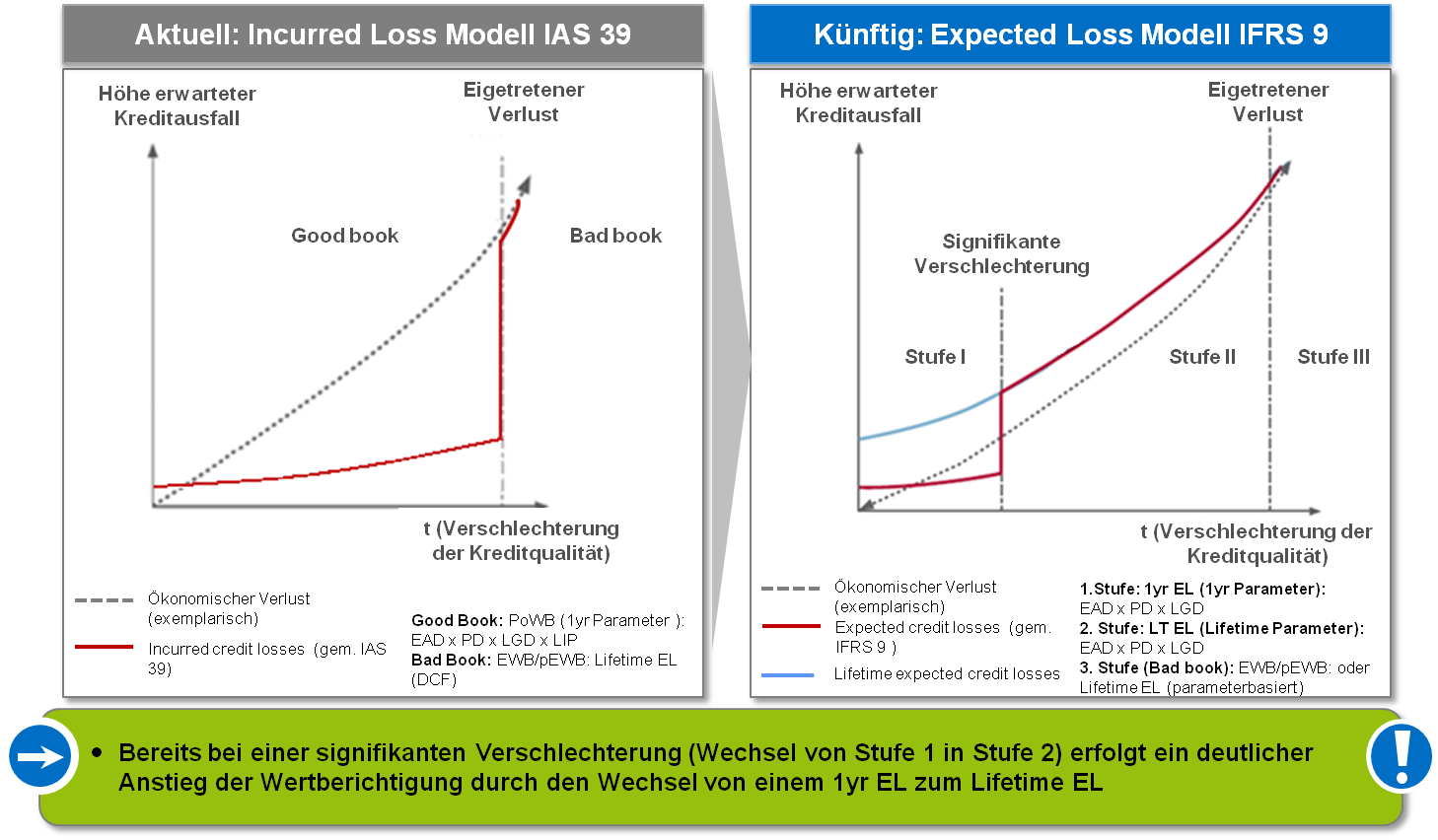

Under the IFRS 9 ‘expected loss’ model, a credit event (or impairment ‘trigger’) no longer has to occur before credit losses are recognised An entity will now always recognise (at a minimum) 12month expected credit losses in profit or loss Lifetime. (a) the interaction of paragraph 9 of IFRS 15 with paragraphs 47 and 52 of IFRS 15 on estimating variable consideration (Examples 2–3);. The PRA letter is helpful in providing specific guidance to assist banks in navigating the significant judgements required to comply with IFRS 9 in uncertain conditions and follows similar statements from the European Securities and Markets Authority (ESMA) and the European Banking Authority (EBA) this week.

IFRS 9 is an International Financial Reporting Standard (IFRS) published by the International Accounting Standards Board (IASB) It addresses the accounting for financial instruments It contains three main topics classification and measurement of financial instruments, impairment of financial assets and hedge accounting. En with and without the application of transitional arrangements for IFRS 9 or ECLs The aim of these Guidelines is to ensure consistency and comparability of the data disclosed by institutions during the transition to the full implementation of the new accounting standard and to foster market discipline. IFRS 9 requires that a bank should measure (both lifetime and 12month) ECL in a way that reflects an unbiased and probabilityweighted amount that is determined by evaluating a range of outcomes;.

Learn more at http//wwwpwccom/ifrs9 There is a common perception that IFRS 9 Financial Instruments will not have a big impact on Corporates in this vide. December 17 In depth IFRS 9 impairment significant increase in credit risk The introduction of the expected credit loss (‘ECL’) impairment requirements in IFRS 9 Financial Instruments represents a significant change from the incurred loss requirements of IAS 39. 17 IFRS 9 replaces most of the guidance in IAS 39 and has reduced the number of classifications for financial instruments IFRS 9 applies a single classification and measurement approach to all.

Deutsche Bank (XETRA DBKGnDE/NYSE DB) today published its IFRS 9 Transition Report This provides transparency on Deutsche Bank’s implementation of IFRS 9, which is mandatory for reporting under International Financial Reporting Standards and has replaced IAS 39 as of January 1, 18 IFRS 9 introduces new requirements on how an entity should classify, measure and reflect impairments to financial instruments. IFRS 9 IFRS 9 Financial Instruments brings fundamental change to financial instrument accounting as it replaces IAS 39 Financial Instruments Recognition and Measurement Our specialists explain the new expected credit loss model for financial asset impairment, the impact of the business model on accounting and the consequences of fewer categories for assets. IFRS 9 accounting change confirmed As expected, the IASB confirmed the accounting for modifications of financial liabilities under IFRS 9 That is, when a financial liability measured at amortised cost is modified without this resulting in derecognition, a gain or loss should be recognised in profit or loss The gain or.

IFRS 9 soll zukünftig IAS 39 als Standard für die Bilanzierung von Finanzierungsinstrumenten ablösen Wie IAS 39 behandelt somit auch IFRS 9 alle Themen mit. In order to determine the appropriate classification category under IFRS 9, entities must assess whether their financial assets meet the SPPI test at the date of initial recognition While financial assets that contained nonclosely related embedded derivatives under IAS 39 are more likely to fail this test, it is important that the contractual. An IFRS 9 Glossary of Common Terms and Abbreviations The IFRS 9 Glossary is a collection of terms relevant for the implementation of the IFRS 9 reporting standard The glossary incorporates and extends the list of terms included in the standard (Appendix A, Defined Terms), The glossary links to more detailed articles that offer more indepth discussions and (where applicable) mathematical.

IFRS 9 – Financial Instruments „Der Weg zu einer erfolgreichen Implementierung der neuen Anforderungen“ Bereits seit den ersten Diskussionen im Jahr 08, aber spätestens seit der Veröffentlichung des „IFRS 9 – Financial Instruments“ durch das IASB im Juli 14 steht fest – die neuen Bilanzierungs und Bewertungsregelungen für finanzielle Vermögenswerte stellen einen Umbruch in der Bankenlandschaft dar. IFRS 9 Financial Instruments issued on 24 July 14 is the IASB's replacement of IAS 39 Financial Instruments Recognition and Measurement The Standard includes requirements for recognition and measurement, impairment, derecognition and general hedge accounting. IFRS 9 contains an option to designate, at initial recognition, a financial asset as measured at FVTPL if doing so eliminates or significantly reduces an ‘accounting mismatch’ that would otherwise arise from measuring assets or liabilities or recognising the gains and losses on them on different bases Financial assets designated at FVTPL.

December 17 In depth IFRS 9 impairment significant increase in credit risk The introduction of the expected credit loss (‘ECL’) impairment requirements in IFRS 9 Financial Instruments represents a significant change from the incurred loss requirements of IAS 39. The IFRS ® Foundation is a notforprofit international organisation responsible for developing a single set of highquality global accounting standards, known as IFRS Standards Our mission is to develop standards that bring transparency, accountability and efficiency to financial markets around the world Our work serves the public interest by fostering trust, growth and longterm. The way we present the Allianz Group financial statements will change in the future Two new accounting standards, IFRS 17 for insurance contracts and IFRS.

Compliance with the new regulations will already be mandatory for banks and corporates in January 18 Because of dependencies between IFRS 9 and the standard for booking insurance contracts IFRS 17 insurance companies are allowed to postpone the introduction of IFRS 9 until 21 at the latest Your Goals Resultsfocused interpretation. The entity has not invoked the fair value. IFRS 9 Financial Instruments has brought fundamental changes to financial instruments accounting in recent years Our materials will help you understand the requirements of this standard as they relate to your company, as well as offering insights and guidance on the application of IFRS ® Standards.

International Financial Reporting Standard 9 (IFRS 9) is a new accounting standard set to replace International Accounting Standard 39 (IAS 39) It introduces a new approach to accounting for financial instruments and is expected to become effective in December 18 The three main areas covered by IFRS 9 are Classification and measurement of financial instruments. IFRS 9, as amended, introduces a logical approach for the classification of financial assets, which is driven by cash flow characteristics and the business model in which an asset is held and a new, expectedloss impairment model that will require more timely recognition of expected credit losses. IFRS 9 states that firms shall apply a definition of default consistent with the definition used for internal credit risk management purposes However, there is a rebuttable presumption that a default does not occur later than when the instrument is 90 days pastdue.

The implementation of IFRS 9 as of January 1, 18, led to a decrease of Deutsche Bank’s Shareholders’ equity of € 671 million including a tax benefit of € 199 million Regulatory capital decreased by € 393 million due to a lower deduction of expected credit. IFRS 9 replaces IAS 39’s patchwork of arbitrary bright line tests, accommodations, options and abuse prevention measures for the classification and measurement of financial assets after initial recognition with a single model that has fewer exceptions. IFRS 9 is effective for annual periods beginning on or after 1 January 18 with early application permitted IFRS 9 specifies how an entity should classify and measure financial assets, financial liabilities, and some contracts to buy or sell nonfinancial items.

The IFRS Foundation provides free access (through Basic registration) to the PDF files of the current year's consolidated IFRS ® Standards (Part A of the Issued Standards—the Red Book), the Conceptual Framework for Financial Reporting and IFRS Practice Statements, as well as available translations of Standards This section also provides highlevel and nontechnical summaries for the.

International Financial Reporting Standards Wikipedia

Ifrs 9 Finanzinstrumente Neuregelungen Und Kritische Analyse Schauer Victor Amazon De Bucher

Ifrs 9 Impairment Konkretisierung Der Umsetzungsanforderungen Bankinghub

Ifrs 9 Deutsch のギャラリー

Klassifizierung Und Bewertung Von Finanzinstrumenten Nach Ifrs 9 E Theses

Ifrs 9 Finanzinstrumente Onlinekurs Videoausschnitt Ifu Online Campus De Youtube

Ifrs 9 Verpflichtende Anwendung In Der Eu Ab 18 Rodl Partner

Update Ifrs 9 Impairment Notwendigkeit Zur Fruhzeitigen Vorbereitung Auf Das Neue Verfahren Bankinghub

Ifrs 9 Finanzinstrumente Ifrs Applied

Bilanzierung Von Finanzinstrumenten Nach Ifrs Unter Besonderer Berucksichti Eur 39 99 Picclick De

Ifrs 9 Aus Sicht Der Industrieunternehmen Kpmg Schweiz

Loan Valuations In The Age Of Expected Loss Provisioning Vox Cepr Policy Portal

Ifrs 9 Eroffnet Chancen Fur Die Portfoliostruktur

Credit Impairment Under Ifrs 9 For Banks

Ilyassaeed Ilyas Saeed Chartered Accountants Ias Ifrs Summary Series Financial Instruments Ifrs 9 Ifrs9 Ilyassaeedcharteredaccountants T Co Amwez10nvr

Ifrs 9 General Hedge Accounting Deloitte Deutschland

Ifrs 9 Als Nachfolgestandard Des Ias 39 Grin

Ifrs 9 General Hedge Accounting Deloitte Deutschland

International Financial Reporting Standard 9 Wikipedia

Neue Internationale Regelungen Zur Klassifizierung Und Finanzinstrumenten Ifrs 9 Saarbrucken 19 Mai Martin Kopatschek Partner Pdf Free Download

Farr Checkliste 16 Anhang N Ifrs 8 A 19 Deutsch Neu Ebay

Bilanzierung Nach Ifrs 9 Im Uberblick Deloitte Deutschland

Ifrs

Www Drsc De App Uploads 17 03 50 01a Ifrs Fa Ershfa48 Idw Pdf

Www Drsc De App Uploads 17 03 50 01a Ifrs Fa Ershfa48 Idw Pdf

Download E Book How To Model And Validate Expected Credit Losses For Ifrs 9 And Cecl

Ifrs 9 Summary Requirements Changes Deloitte Cfr

Ifrs 9 Verpflichtende Anwendung In Der Eu Ab 18 Rodl Partner

Fas Ag Ias 39 Finanzinstrumente Ansatz Und Bewertung

Www Drsc De App Uploads 17 03 50 01a Ifrs Fa Ershfa48 Idw Pdf

Iasb And Regulators Highlight Ifrs 9 Ecl Requirements In Coronavirus Pandemic Pagetitlesuffix

Fas Ag Einfuhrung Von Ifrs 9 Anderungen Der Bilanzierung

Ifrs 9 Finale Fassung Zur Bilanzierung Von Finanzinstrumenten Rodl Partner

International Financial Reporting Standards Ifrs Isbn 978 3 527 9 Fachbuch Online Kaufen Lehmanns De

Ifrs 9 Finanzinstrumente Hedge Accounting

Ifrs 9 Teil 1 Analyse Der Fehler Ias 39 Ifrs 7 Ifrs 9 Teil 1 Ebook Klamra Karl Heinz Amazon De Kindle Shop

Ifrs 9 Und Ecl Cva Services Gmbh

Ifrs 9 Ansatz Ausbuchung Und Modifizierung

Www Wiwi Uni Muenster De Fcm Sites Fcm Files Homepage Praxis Foerderer Schmalenbach Arbeitskreis Financial Instruments Nach Ifrs 9 Pdf

Bilanzierung Aktuelles Zur Internationalen Rechnungslegung Ifrs 9 Icon Wirtschaftstreuhand Gmbh

Www Kpmg At Uploads Media An 14 06 Pdf

Ifrs 9 Financial Instruments Reporting Solutions November 17

Zbam9t27vrui5m

Financial Assets Under Ifrs 9 The Basis For Classification Has Changed o Australia

Product

Ifrs 9 Impairment Practical Implications Protiviti United States

Ifrs 9 Kpmg Germany

Fas Ag Ifrs 9 Finanzinstrumente

Ifrs 9 Eine Zusammenfassung Verovis

Ifrs 9 Financial Instruments

Disclose Update Ifrs 9 Betrifft Alle Ifrs Anwender

Ifrs 9

Ifrs 9 Financial Instruments Overview

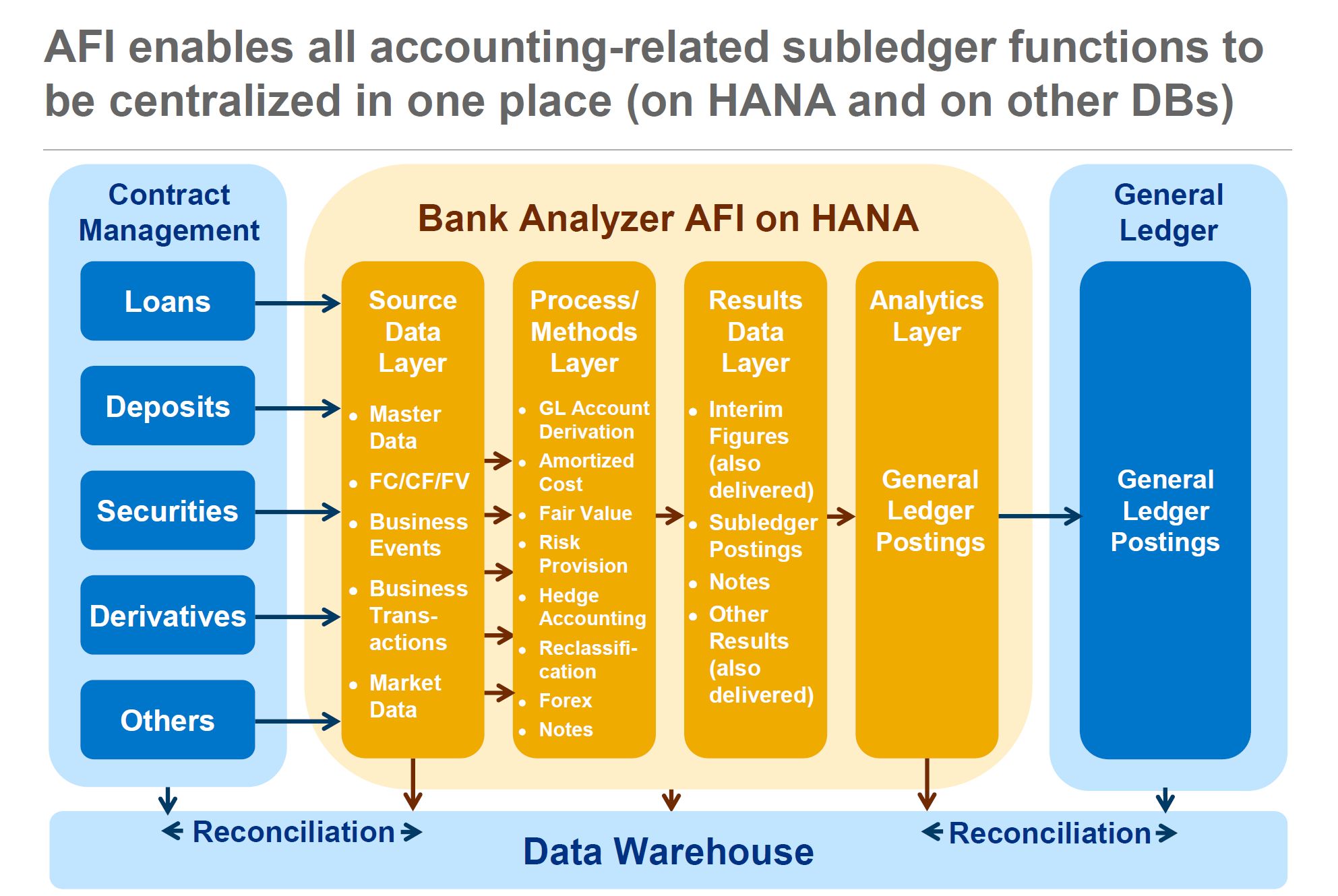

Sap Bank Analyzer Afi

Ifrs 9 Impairment Konkretisierung Der Umsetzungsanforderungen Bankinghub

Das Neue Wertminderungsmodell Nach Ifrs 9 Und Die Damit Grin

Ifrs 9 Aus Sicht Der Industrieunternehmen Kpmg Schweiz

Zbam9t27vrui5m

Www Bundesbank De Resource Blob 71c8cf60bc9784d052a5d5afd810f0d1 Ml 19 01 Ifrs9 Data Pdf

Www Drsc De App Uploads 17 03 50 01a Ifrs Fa Ershfa48 Idw Pdf

Ifrs 9 Impairment Practical Implications Protiviti United States

Die Bewertungskategorien Des Ifrs 9 Grin

Ifrs 9 Fur Industrie Und Handelsunternehmen Deloitte Deutschland Audit

Ifrs 9

Validation Of Ifrs 9 Models

Prepare Ifrs 9 Ecl Model Using Both General And Simplified Approach By Basit

How To Make Sense Of Transition To Ifrs 9 Expected Credit Loss Model Ey Global

Read Ifrs 9 And Cecl Credit Risk Modelling And Validation Online By Tiziano Bellini Books

Ifrs 9 Eine Zusammenfassung Verovis

Ifrs 9 Impairment Ein Blick Uber Den Tellerrand Der Lifetime Loss Modellierung Bankinghub

Www Db Com Ir De Download Deutsche Bank Ifrs 9 Ueberleitungsbericht Pdf

Www Fas Ag De Fileadmin User Upload Knowledge Studien Fair Value Bilanzierung Von Kreditinstituten Pdf

Neue Internationale Regelungen Zur Klassifizierung Und Finanzinstrumenten Ifrs 9 Saarbrucken 19 Mai Martin Kopatschek Partner Pdf Free Download

Heads Up Iasb Completes Its Project On Accounting For Financial Instruments Under Ifrs 9

Ifrs 9 Finanzinstrumente Youtube

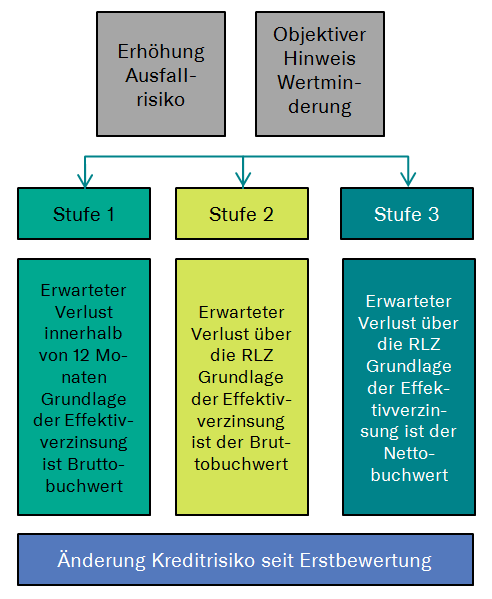

Das Kreditrisiko Im Stufenkonzept Nach Ifrs 9 Grin

Konzernanhang Puma Annual Report 17 Forever Faster Puma

Ifrs 9 Overview For All Accountants

Disclose Update Ifrs 9 Betrifft Alle Ifrs Anwender

Update Ifrs 9 Impairment Notwendigkeit Zur Fruhzeitigen Vorbereitung Auf Das Neue Verfahren Bankinghub

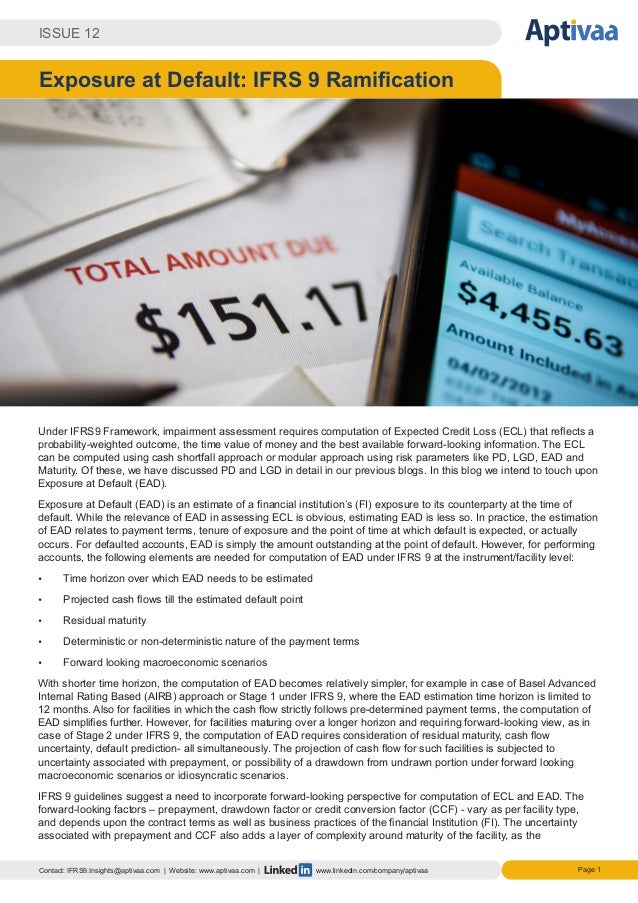

Blog 16 12 Ead Ifrs 9 Ramifications

New Ifrs 9

Ifrs 9 Solution For Sap Trm Fam Compiricus

Das Wertminderungsmodell Des Ifrs 9 Im Vergleich Zum Ias 39

Eur Lex Europa Eu Legal Content De Txt Pdf Uri Celex 316r67 From Ro

Ias 39 Ifrs 9 International Financial Reporting Standards Impairment International Accounting Standards Board Angle Text Png Pngegg

Fas Ag Ifrs 9 Finanzinstrumente

Ifrs 9 Impairment Konkretisierung Der Umsetzungsanforderungen Bankinghub

Ifrs 9 Implikationen Fur Die Kapitalanlage

Ifrs 9 Und Ecl Cva Services Gmbh

Ifrs 9 Finanzinstrumente Neuregelungen Und Kritische Analyse Schauer Victor Amazon De Bucher

Bilanzierung Nach Ifrs 9 Im Uberblick Deloitte Deutschland

Ifrs 9 Finanzinstrumente Institut Fur Rechnungslegung

Ifrs 9 Im Ubergang Von Theorie Zu Praxis Rodl Partner

Fas Ag Ifrs 9 Finanzinstrumente

Ifrs 9 Impairment Ein Blick Uber Den Tellerrand Der Lifetime Loss Modellierung Bankinghub

Die Reform Des Ias 39 Durch Den Ifrs 9 Kosakowski Florian Amazon De Bucher

Www Iasplus Com De Publications German Publications Other Ifrs 9 Praxisleitfaden Fuer Finanzdienstleister File

Bilanzierung Nach Ifrs 9 Im Uberblick Deloitte Deutschland

Hedge Accounting In Industrieunternehmen Nach Ifrs 9 Rechnungslegung Dettenrieder Dominik Amazon De Bucher

Kpmg Nigeria Auf Twitter Classification And Measurement Of Financial Assets In The Scope Of Ifrs 9 Africaifrsacademy T Co Huhoia3yok